The biggest concern of most any retiree is the answer to their question, "How long will my money last in retirement?" Clearly, outliving one's money at age 80 and being destitute is a most unpleasant scenario. So let's look at five retirement strategies that will address how will my money last in retirement.

Retirement Strategies - Do Not Invest Too Conservatively

The most conservative investments also have the lowest interest rates. So if you sit with money in the bank earning 1%, you are much more likely to need to spend the principle because your funds have insufficient earnings.

Paradoxically, many people think that money in the bank couldn't be safer. In fact, earning a low rate exposes your principal to faster exhaustion as you will need it for living expenses. It is far better to think long-term and earn a higher rate. This does not mean you need to take risk with your assets. But keeping more than 10% of your funds in the bank is one of the worst retirement strategies.

For example, even in this low-interest rate environment at the end of 2016, one of many excellent retirement strategies is to purchase the preferred shares of major banks and earn 5%. If you are worried that Bank of America or Wells Fargo may go bankrupt, then these securities are not for you. But if you understand that these banks are too big to fail and no matter what happens in the economy, these banks will be sustained by the US government, then you can feel pretty secure with a good return and preservation of your principal. Does it seem to you that earning 5% rather than 1% will go a long way to address the concern of how long will my money last in retirement?

One page "invest like the rich" cheat sheet provides short explanations of how the rich investment differently. You don't need to be rich to copy what they do. Download now.

Retirement Strategies - Do Not Invest Short Term

Assume that you retire at age 65 and your spouse is also 65. There is a 42% chance that one of you will live to age 90 or beyond. Therefore, one must prepare for a retirement that spans 25+ years. Does it make sense to choose investments with the 12-month duration when you need your money to last 25 years? Or, does it make sense to select investments with the time horizon that matches your financial requirements?,

Almost always, longer-term investments will provide a better yield than shorter term investments. One of the most overlooked retirement strategies is to buy bonds that last as ling aas you do (20-40 years) and to stay away from short-term low-yield fixed income investments. Just look at this table of AA corporate bond rates:

| Corporate Bonds | |

| Maturity | Yield |

| 2yr AA | 1.27 |

| 2yr A | 1.33 |

| 5yr AAA | 1.91 |

| 5yr AA | 2.04 |

| 5yr A | 2.1 |

| 10yr AAA | 2.86 |

| 10yr AA | 2.86 |

| 10yr A | 3 |

| 20yr AAA | 3.61 |

| 20yr AA | 4.12 |

| 20yr A | 4.18 |

If you need your money to last longer, would it make sense to purchase the 20-year AA-rated bond for 4.12% and earn 224% more income than a two-year AA-rated bond? Which do you think will best address the concern of how long will my money last in retirement?

Retirement Strategies - Own Equities

Some people mistakenly think that wealthy people will naturally take more risk with their money. However, this thinking is an error.

If you have $10 million and put it in the bank at 1%, you will have $100,000 a year of interest income. And you decide that $100,000 is a sufficient amount of income on which you can live comfortably. Therefore, such a rich person can invest poorly and still have adequate income.,/p>

But let's say you don't have $10 million. Let's say you have $500,000. If you invest that at 1%, your income is $5000 annually. Can you live on $5000 a year?

Therefore, people of more modest means must invest more aggressively because they must earn a higher return on their money. How Long Will My Money Last in Retirement? Not very long at 1% interest! It's only rich people who can invest poorly and still have sufficient income. Over long periods of time, history shows that stocks have provided a better return than other assets. The key is to be a long-term investor.

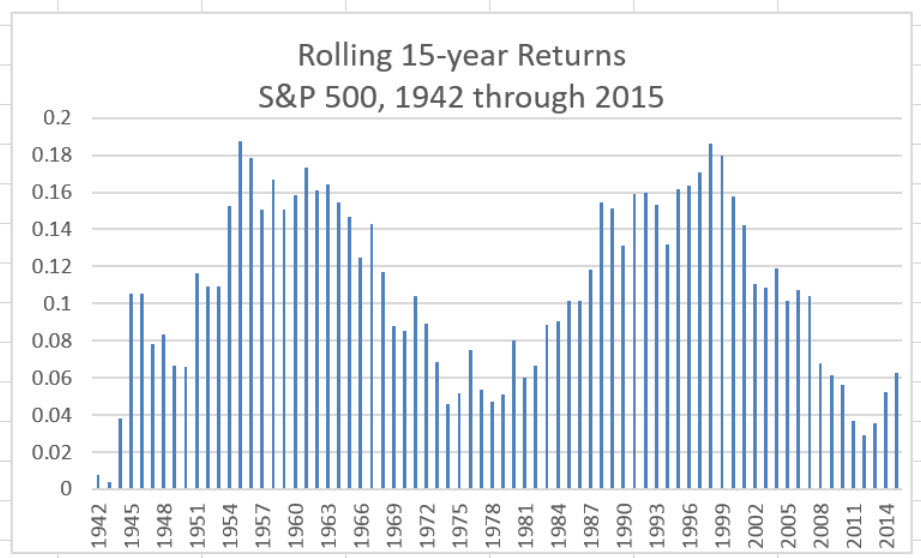

There has been no 15-year period when an investment in the S&P 500 would have lost money. So if you believe that history repeats itself, it's a fair assumption that if you invest in the market index and leave the money alone for 15 years, you will have a positive return on your money. Additionally, that positive return will be greater than the return you would have had in other assets. Let's take a look.

The chart shows the following: if you invested money in 1928, just before the Great Depression and then looked at your balance 15 years later, you would've had a very small return, less than 1% a year. However, you would not have lost nominal principal. If you do the same thing each year to see how much you would've earned over the previous 15 years by investing in the S&P 500 index, you see your return represented by each bar on the chart. Notice that none of the bars dip below zero. That means you have a positive return every 15-year period. And the percentage return for each period is displayed on the left axis. If you average all the 15-year returns since 1928, the average is 10.73% annually. Would that return help ease your concern about how long my money will last in retirement? Of course, keep in mind that past returns do not guarantee future results. However, in this author's experience, history repeats itself.

Of course, keep in mind that past returns do not guarantee future results. However, in this author's experience, history repeats itself.

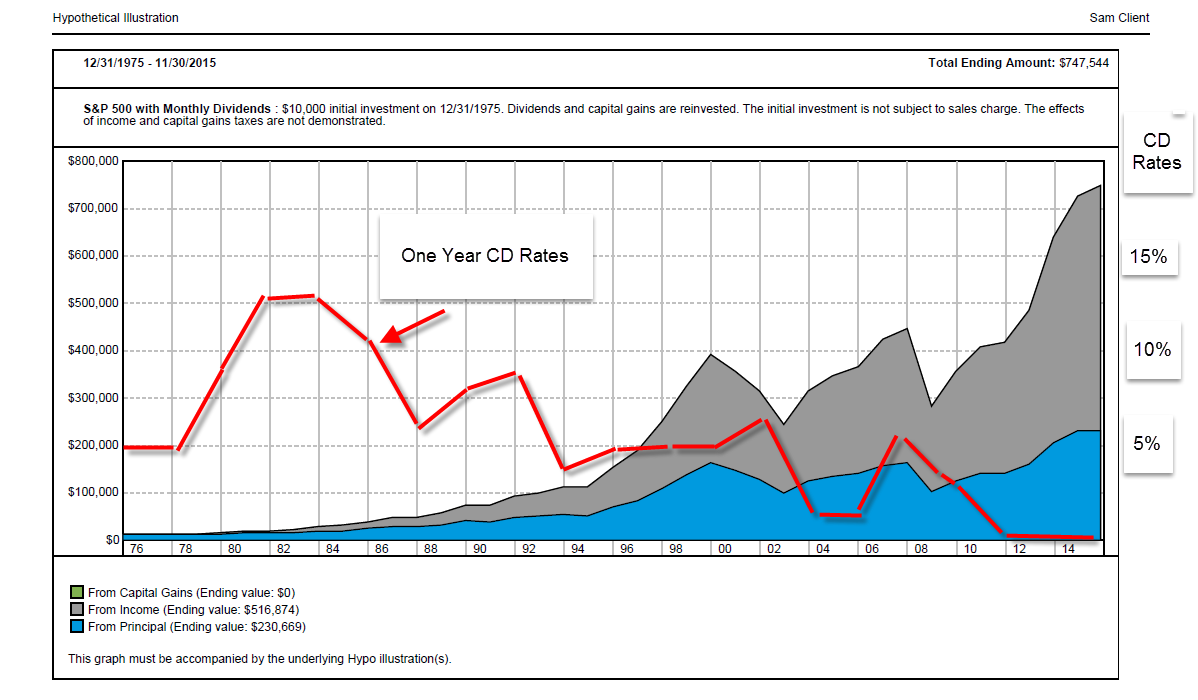

There is another more important reason to own stocks in retirement. The increases in dividends have been persistent. And one of the overlooked retirement strategies is to have increasing income over time. If you want to allay the concern of how long will my money last in retirement, you need to have a source of income that grows along with your cost of living.

Dividend increases have been immune to the decline in interest rates. Assume that you retired in 1982 at the peak of the interest rate cycle. At that time, depositors received 12+% interest at the bank. Then, year after year, the interest rates went down, down and down to today's level where you get 1% of the bank (the red line below). During the same period, dividends from the stocks in the S&P 500 increased with persistency (the gray area below).

Retirement Strategies - Don't Pay Income Tax

It is easier to avoid paying income tax in retirement than at any other time during your life. In addition to the regular tax breaks, there are six special senior tax breaks. Unfortunately, most people are not aware of them and too many accountants are too narrowly focused to advise you on their use. And since taxes are significant (up to 39.6% of your marginal income), you must reduce them to address how long will my money last in retirement.

We wrote a recent post on this topic explaining the six special senior tax breaks. The post illustrates an example of a retired couple with $100,000 of income who pay no tax. Study that post and take a copy to your accountant so that he can help you apply every possible tax break available.

As an example, you may be surprised that most retirees can avoid paying tax on Social Security benefits. This takes some planning most accountants overlook providing this advice. By pre-planning and selecting the right investments you can reduce or eliminate the tax on your Social Security income.

Retirement Strategies - Aggressively Minimize Expenses

This single most powerful act you can take to determine how long will my money last in retirement: aggressively minimize your expenses. I don't just mean eating out less often or buying one less pair of shoes. I mean reducing the big expenses.,

Have you considered moving to a lower cost area? Or have you considered moving out of the United States? These are viable and sensible options for those who reach retirement age with insufficient assets. While you may need $5000 per month to live comfortably where you reside currently, you can live on half that amount in Belize (no need to learn a foreign language, the official language is English). Millions of retirees relocate abroad because of the lower cost of living. This reduces financial strain and worry and thus provides increased quality of life. The significant issue is medical care, as Medicare is not available to you outside of the US.

Imagine, however, living in a town where you can either walk everywhere, take a taxi for two dollars, rent a nice home for under $1000 per month and dine out every night for eight dollars. Sound like a good way to mitigate your concern of how long will my money last in retirement?

We like this article at Investopedia, "8 Countries Where $200K in Retirement Savings Will Last 30 Years."

Retirement Strategies - Make the Right Health Care Decisions

Don't blow your retirement nest egg by leaving significant risks uninsured. Get the right healthcare.

Studies that show a retiree will spend over $200,000 in medical costs during their retirement. I find that to be hype. I don't think it is true. I think that when a retiree has the right type of health insurance, significant out-of-pocket expenses can be avoided. I am not a health care insurance expert but it seems clear to me that a good Medicare Advantage plan will trump traditional Medicare.

I was a financial advisor to retirees for more than a decade. I was privy to personal financial information of over 2000 retirees. Many retirees in my geographic area belong to a Medicare HMO through Kaiser (see details below). While similar plans are not necessarily available everywhere in the country, I assume comparable coverage can be obtained, maybe at a higher monthly premium.

Below you can see the coverage provided and that the out-of-pocket cost is capped. Furthermore, because this is an HMO, the plan provides convenience with all medical care coordinated and delivered at the same facility. I cannot understand why a retiree would choose traditional Medicare where you must coordinate your own care among unrelated doctors, get deductible and copayment bills in the mail, pay for separate Medigap insurance and deal with a host of unnecessary complications.

I believe the choice of traditional Medicare, even in combination with a Medigap policy, can leave significant holes in your coverage. Alternatively, Medicare Advantage plans tend to be all-inclusive with a cap on annual out-of-pocket expenses.

| Premiums and Benefits | Kaiser Permanente Senior Advantage HMO |

| DESCRIPTION | YOU PAY |

| Monthly Premium | $86 |

| Annual Maximum Out-of-Pocket | $4,400 |

| Annual Deductible | None |

| Doctor Office Visit | $35 Primary / $35 Specialist |

| Emergency Room | $75 |

| Urgent Care | $35 |

| Preventive Services | No charge |

| Inpatient Hospitalization | $280 per day for days 1–7 of your stay. |

| Thereafter, no charge for the remainder of your stay. | |

| Outpatient Surgery | $250 |

| Skilled Nursing Facility | $0 per day for days 1–20 |

| $50 per day for days 21–100 | |

| Up to 100 days per benefit period | |

| Lab, X-ray, Imaging | $35 Lab, $55 X-ray, ultrasound, |

| $205 MRI, PET, CT scans | |

| Durable Medical Equipment | 20% coinsurance |

| Ambulance Service | $200 copay |

| Per one-way trip |

Retirement Strategies - Get Protected for Long Term Care

The need for long-term care could easily bankrupt anybody. A nursing home stay exceeds $80,000 a year in many areas of the country. If you don't have sufficient assets or income to bear this cost for up to five years, then it is important you get insurance. How long will my money last in retirement without protection for long-term care expenses? Not long.

The insurance is not inexpensive. However, there are recent innovations that permit you to get coverage at a less painful cost.

For example, there are now combination policies where you make one single deposit of say $50,000 or $100,000 and receive benefits several times that amount. The benefit will either pay off as life insurance to your beneficiaries or can be used for your own long-term care expenses during your lifetime.

Then of course, there is the state managed benefit of Medicaid. Medicaid is designed for people who have little to no financial resources. However, many elder care attorneys show modestly wealthy retirees how to organize their financial affairs so that the retiree can qualify for Medicaid coverage. So if that possibility appeals to you, find an elder care attorney in your area that can explain this option.

Summary: How Long Will My Money Last in Retirement

If you keep thinking about making your money last in retirement the same ways, you likely will continue to worry or believe a financially comfortable retirement is not possible. But if you make the changes discussed in this post, you will find that previously unforeseen solutions are available for a great retirement.

Nice one to read about very good blog

Problem with HMO's, you cannot choose your doctor or hospital. Also you cannot go to a specialist without a referral. If you have a serious chronic health problem or need surgery; this can cost you your health or life. No thank you.

Your comments are not always true as this caries from HMO to HMO.

I am able to go directly to a specialist without a referral.

I never ever have to complete any forms.

All medical records instantly accessible to every doctor.

Many other advantages but it's a personal choice and you cannot generalize.