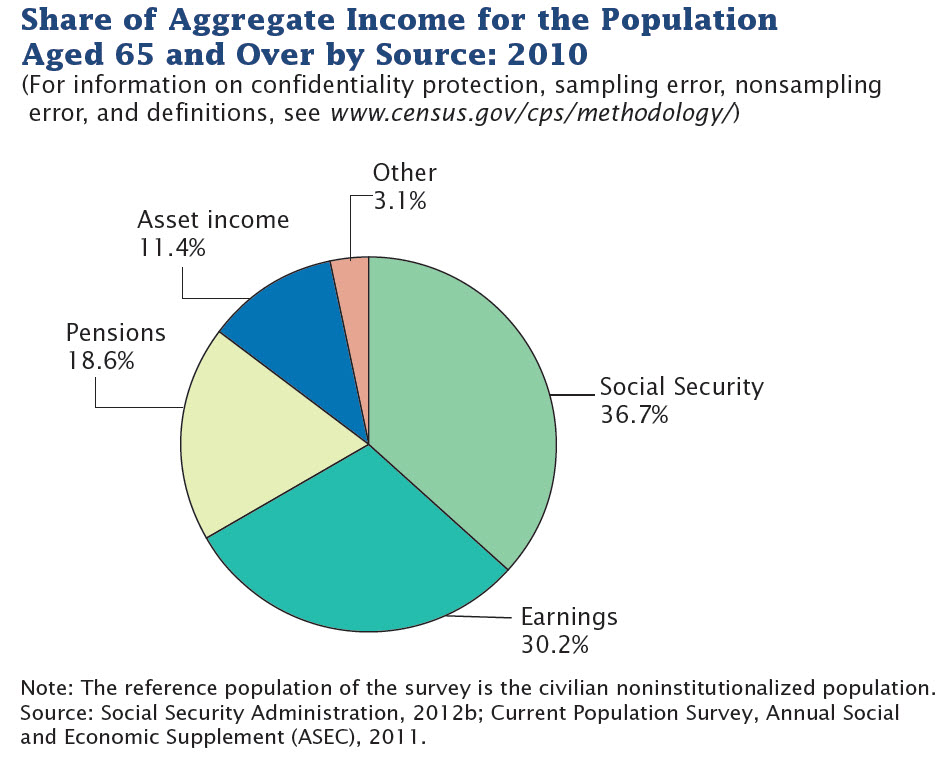

According to the US Census Bureau, these are the sources of retirement income and proportions thereof. These are not, however, the best sources of income for retirees. The best retirement income sources are those that you control.

Controllable and Uncontrollable Income Sources

Note that 59% of the retirement income sources are not within your control (e.g. Social Security income and pension income). Therefore, I won't address these uncontrollable sources. Let's address the 41% of retirement income sources you can control. That's your objective - to have a large percentage of retirement income from sources you control.

Let's also note that the portion of retirement income you can control may be increasing as employer-provided benefits have been on the decline (and thus the rise of self-funded 401k plans). Additionally, the more recent data shows that more people are working at older ages thereby increasing the income under their control during retirement years.

In summary, people of retirement age will get a smaller percentage of their income from their Social Security payout and pensions and a larger share from wages and investments.

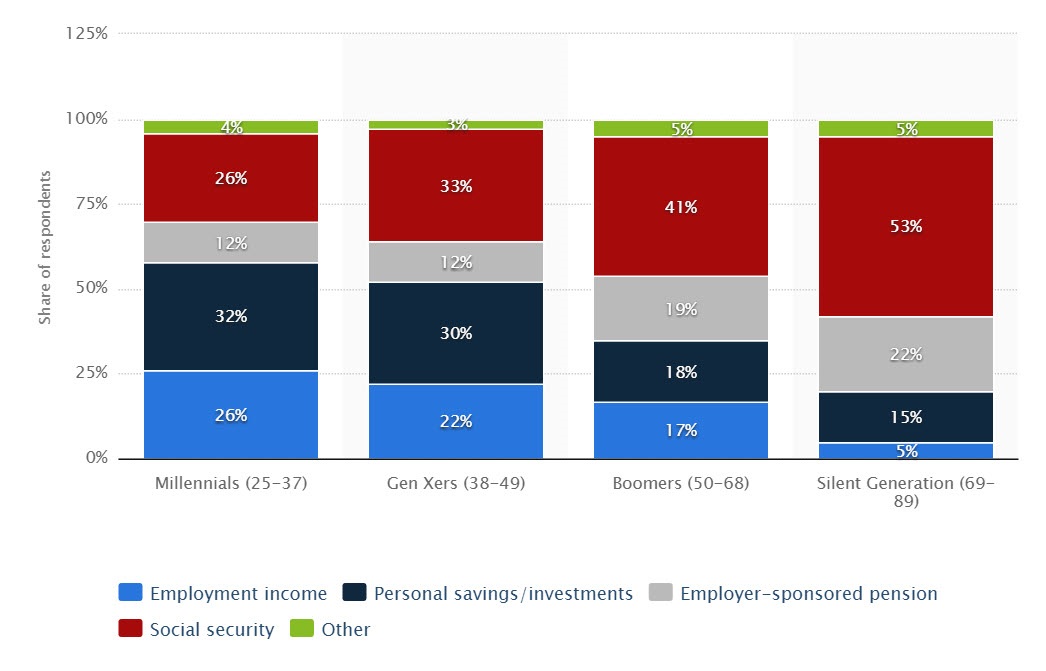

EXPECTED INCOME SOURCES for Retirement

We already saw from the pie chart above that current retirees control 45% of their income, and that is expected to rise, out of necessity. Older respondents to the above survey have unrealistic expectations before they retire.

As you see from above, the younger the respondent, the more realistic their expectation of income sources. Millennials expect 58% of their retirement income to come from employment and personal savings/investment (IRAs, 401ks, Roth IRA, employer retirement plans, etc). That boomers expect only 35% of retirement income to come from controllable sources is unrealistic. Already retirees get 41% of income from controllable sources, most of that being earnings. Boomers can expect to work more, not less, than those already retired. They may be in for a cruel awakening.

Those within ten years of retirement may be negatively shocked to learn that more of their retirement income will depend on their prowess at working (including self-employment) and investing.

This post goes beyond the basic advice of using a retirement calculator to estimate your income needs, what your savings need to be, retirement planning basics, how to construct your portfolio or investing for dividends. We have covered these topics in earlier posts and here we present more advanced ideas.

Working During Retirement Years

The trend to work at later ages is increasing. According to the Pew Research Center:

"In May, 18.8% of Americans ages 65 and older, or nearly 9 million people, reported being employed full- or part-time, continuing a steady increase that dates to at least 2000 (which is as far back as we took our analysis). In May of that year, just 12.8% of 65-and-older Americans, or about 4 million people, said they were working."

We intuitively would guess that people are working longer as we know from a multitude of media reports that people have under-saved for retirement. Therefore, the obvious choice is to keep working.

However, there are factors which make gainful employment for older workers problematic:

- age discrimination

- lack of digital skills

Because many older workers may be uncompetitive to get jobs, we recommend income from self-employment options. We wrote some posts on self-employment opportunities for those without special skills.

Best Income Sources - The Right Retirement Investments

As to investing, my experience as a financial advisor shows me that most people are underinvested, i.e. they get a poor return on their assets. Their best retirement income opportunities can significantly boost investment performance. However, as I will disclose, financial advisors often do not mention these sources and the general public is financially ignorant. The rich earn more on their assets for two reasons. They can take advantage of investments with larger minimum requirements than most investors can afford and the rich are also better informed.

There are many sources of investment income. In fact, within a 401k there are choices such as equity mutual funds, bond mutual funds, and real estate investment trusts. Then we could further divide mutual funds into open-end funds, closed-end funds and exchange-traded funds (ETFs). Within bonds, we have Treasury securities, federally backed mortgage notes, corporate bonds and tax-free bonds.

Additional retirement income sources would include retirement annuities: traditional fixed annuities, variable annuities, and equity-indexed annuities. To supply any detail in one article would be overwhelming so in this blog, we have devoted at least one post to each of these retirement income sources, and you can locate these posts using the category listing at https://retirementincome.net

All of the above are readily sold by eager financial advisors and insurance agents to earn a commission. But what about the best retirement income sources for which they cannot earn a commission? These salespeople can only sell what their employing companies permit them to sell.

You can steer clear of these salespeople. Let me give you a simple formula that will beat 98% of their recommendations.

Understand that of what appears to be a huge menu of investment alternatives, there are only three investments: stocks, bonds and cash (i.e. places to store cash such as bank accounts and money market funds). EVERY other investment financial advisors sell is some combination, synthesis or derivative of these three investments. The exception would be real estate (i.e. REITs and direct participation programs).

The reason that Wall Street manufactures so many investments based on only three components: the opportunity to charge you more. For example, mutual funds are a collection of stocks, bonds, and cash. And for owning the fund, you typically pay 1%++ annually in fees.

Since the three components comprise almost every packaged investment product, would it make sense only to own those three and avoid a lifetime of fees?

Here's your simple strategy.

For the portion of money you want to have in the stock market, you buy an S&P index fund from Vanguard -- annual fee about 1/6 of 1% (For low fees, Vanguard is your best choice. Avoid seemingly low-fee offerings from Fidelity, AARP or Charles Schwab). The S&P 500 has a higher return than most actively managed funds in most years.

For the portion you want more secure, you invest in bonds, not bond funds. You buy individual bonds and hold them to maturity. The bonds you buy should match your remaining life expectancy. Buy 30-year bonds if you plan to be alive for 30 years. You pay no annual fees to hold individual bonds. (Below, I cover alternative income investments for generating income that you would use to replace bonds).

The last little bit you keep in a checking account for near-term liquidity needs -- target not more than 12 months requirement.

The Best Income Sources for Retirees

The best sources of retirement income are likely unfamiliar to you, often called alternative investments.

Be cautious about your thinking. Most people believe new opportunities are risky opportunities. This thought is inaccurate.

I have a friend who has jumped out of an airplane over 500 times. He views this activity as one of the most exciting ways to spend a day. I consider this activity as one pursued by people with a death wish who are thrill-seeking crazies. My opinion, of course, is inaccurate when you know the facts: In 2013, there were 3.2 million jumps out of airplanes in the United States, and only 24 people were killed in the process. Of 10 million car accidents per year, according to a report by the US Department of Transportation, about 40,000 of these accidents result in fatalities. Driving a car is infinitely more dangerous than jumping out of a plane (with a parachute, of course).

So please open your mind to learn and resist the unfounded and incorrect thoughts about risk. Let your brain not your emotions be your guide.

Best Income Source #1-Make Money Just Like Your Bank

Foolish people go to their bank and deposit substantial sums to earn 1%. I say this is foolish because:

- they pay tax on the 1%

- if inflation is 2%, they have lost purchasing power, the same as losing money

Your banker is much smarter. He pays you 1% and turns around and lends the money at 4% to someone buying a home. So the bank gets four times as much as they pay you. Who's the smart one in this arrangement?

You can do the same as your bank yet earn even more. Your bank is constrained by federal mortgage insurance regulations when they lend money on a home. If you loan money secured by a home, you are not restricted by these regulations. You can earn 8% rather than 4%.

Let's look deeper.

Let's say you have $300,000 equity in your home. How much do you earn on that equity? You earn 0%. Someone likely taught you that equity in your home is a good thing. It's a stupid investment as it earns 0%. If this is not immediately clear, you can read our post on why home equity is a bad asset to own.

For simplicity, say you could take that $300,000 and loan $100,000 each to three homeowners in your town. Which seems safer--having $300,000 of equity in your home that maybe gets destroyed by an uninsured loss (e.g. flood which is not covered by your homeowner's policy) or having your equity spread across three properties? Let's not forget that the $300,000 lent to these neighbors will generate 8% or $24,000 annually.

The homes against which you lend secure your investment. You only loan to people who have a lot of equity in their homes. So if they don't make their monthly payments to you as scheduled, you can take their home away from them. Don't worry; you don't ever talk to these people as there are "hard money brokers" licensed by your state that handle these transactions. Here you can learn more about private mortgage loans.

I could write a book on this topic, as many have, and I simplify private mortgage lending for the sake of reader understanding. I have made private mortgage loans for 30 years, and I have never lost a dime or needed to take away anyone's home. Now you know that earning 8% on secured investments is not impossible nor uncommon.

Your financial advisor will never mention this alternative to you because he does not offer it. His firm has decided that they can earn more selling you the fee-laden packaged products produced by Wall Street. You find these alternatives through a hard-money mortgage broker.

Best Income Source #2 - Get Paid When People Die

Since the only sure things are death and taxes, what could be bad about turning these sure things into a profitable opportunity?

Because you are unfamiliar with viaticals or life settlements (two different but similar investments in life insurance policies), you will have negative thoughts. As mentioned before, your brain is programmed to view negatively anything of which you are unaware. You now understand why some people are so dumb--they are already programmed not to learn anything new.

Here's a simple idea. Mr. Jones has a life insurance policy that pays his children $100,000 when he dies. He has a fight with his children that end with the words, "screw you." Since he no longer cares about leaving his kids the $100,000, he wants to use that policy to his benefit, and his life insurance agent tells him how to sell the policy. Who will buy it? You!

Mr. Jonesd is age 70. He is a chain smoker. He has a physical and the doctor estimates that he has eight years to live. You can buy this policy for $40,000. As the owner of the policy, you are the one who collects $100,000 when Mr. Jones dies.

No, this is not a morbid investment. Does everyone die? Yes. Are you betting on Mr. Jone's death? No - he will die when he dies. You are doing the positive act of putting $40,000 in his pocket for an asset that had no value to him.

If Mr. Jones dies in 2 years, your investment turns out to be highly profitable as you converted $40,000 into $100,000 in 2 years. If instead, Mr. Jones lives eight years as estimated by the physician, your annual return on your money is 12% ($40,000 invested that becomes $100,000 in 8 years = 12%). If Mr. Jones lives more than eight years, you will need to wait longer for your money, and you will earn less than 8% a year. The investment is super-safe as you WILL get your $100,000. You just don't know when. And that is why these investments pay 12% (or thereabout) as the term is uncertain.

This investment is not for someone who needs a monthly income and in the truest sense is not one of the best retirement income sources. You could consider it a growth investment. I have already told you about private mortgages which pay interest monthly. Life insurance investments are for funds you can sock away for your later retirement years, funds you don't need at a particular time.

Not Among the Best Income Sources- Private Notes

Over the years, I have seen corporate notes advertised many times. The advertisement says something like "Earn 12 % secured for a two-year term." Let me explain the nature of these notes and why you need to stay away.

Large companies as AT&T, IBM, etc. routinely issue commercial paper. These are short-term notes purchased by money market funds. The corporation pays interest. In March 2017, the 90-day yield on this high-grade commercial paper is 1%. There are smaller companies, less stable companies, who also want to issue commercial paper but the investment is too risky for money market funds to buy. So they place ads in the newspaper to entice not-too-savvy investors.

It is entirely possible you can invest, and everything will work out, and you will get your money back. But it is also entirely possible that the company issuing such notes will be bankrupt by the due date of your investment. My advice is to stay away. Rather, focus on the two best retirement income investments I have detailed previously.

Private mortgage notes secure your investment with a home having a lot of equity. With life insurance policies, your payment is guaranteed by a well-known insurance company.

I think stocks that have income producing dividends or etfs that do is a great way to invest. If you buy quality funds with good paying stocks you get income and if stocks go up you make more. Everyone thinks they live off selling the stocks i think you should try to live on the income and keep stocks.

Best etf funds lists last blog post..Gold double long etf.

I agree people have to make thier own income in retirement. You can not just rely on social security or some 401 k look what happened this year make sure to have some orther income so you always have money.

Interesting to see that social security makes up less than 40% of retirement income. I would think most people's 401k is nothing compared to the government. Is this in the aggregate? Or is this the profile of the typical American? I'm going to have to go with the former. The richest 5% are skewing the results.

I know (historically speaking) stocks have been a great way to go in the U.S. but know I'm convinced that holding a tangible asset like rentals is far safer. It does not surprise me though that rent is one of the least major sources.

Yes, it is important to invest as early as possible. Rentals, Stocks, Bonds, are just some ways you can invest your money.

I'm amazed to see that even when retired people still opt to do part-time work. Isn't retirement supposed to be relaxing and enjoying life?

Plan ahead! Prepare for retirement as early as now. So that when that inevitable time comes, you can just sit back, relax, possibly live off of your investments and enjoy life. You could probably retire earlier too if you get things done right earlier.

Saving money while you're still young can help you when you retire. It is always important not to overspend and spend your money wisely.

Your retirement benefit from a defined contribution or defined benefit plan will be in the form of either a single or a joint and survivor annuity. A single annuity provides benefits until the worker's death, whereas a joint and survivor annuity also provides survivor benefits. To fund these additional survivor benefits, the employer reduces the pension payment. The amount of the reduction sometimes depends on the age difference of the two recipients.

Indians are ready for retirement, but haven’t saved enough. Survey, Aegon Retirement Readiness Survey 2015, reveals that approximate 73% of the respondent form the India believed that they will have to support family members, apart from spouse or partner, financially after retirement.

Very interesting breakdown! It definitely seems as if the average retiree could improve how they save and invest their money based on the income they get from investments.